Digital Assets Report 2025

Jay Wilson, Kibriya Rahman (AlbionVC) Henry Whorwood, Miraj Mistry, and Blanca Valencia (Beauhurst)

In partnership with

Report sections:

Key Statistics

As part of the research we have reviewed 1,426 startups, and made the decision to focus our core analysis on the companies that have raised at least $500k in equity funding. The analysis bench-marks this cohort against the broader fintech sector and the wider UK venture ecosystem, providing context on the maturity and growth trajectory of digital assets as a maturing market.

Active startups UK ecosystem in numbers:

955

aactive digital assets companies

222

raised $500k+ in funding (core focus of this report)

69%

of companies are based in London

A decade of extreme VC power law:

1426

companies

259

raised $500k+ in funding

Top 5

raised £1.05bn out of £2.7bn secured by the sector as a whole

Top 3

raised £894m

Introduction

UK’s edge: the infrastructure bet

As 2025 draws to a close, the United Kingdom stands at a pivotal inflection point for digital assets. With 23 million users—representing 35% of adults and the highest adoption rate in Europe—the UK has as-sembled the foundations of a mature, globally relevant ecosystem. It now has a narrow window of op-portunity to turn this momentum into a lasting competitive advantage.

Our analysis of 1,426 startups over the past decade reveals a striking transformation: the UK digital asset ecosystem has evolved from a nascent, consumer-driven sector into one dominated by B2B business models—over 70% of deals done in 2025 versus just 27% in 2015. These firms are increasingly estab-lished, capital-efficient, and trusted by global customers..

The investment landscape has also matured. The inflow—and subsequent retreat—of international capital has left a market defined by extreme concentration: the top three companies raised £894m of the £2.7bn invested in UK digital asset startups over the past ten years.

Unlike fintech, where the UK is an undisputed global leader, digital assets remain an emerging and more volatile frontier. Yet within it lie clusters of genuine global potential—particularly in areas where London’s centuries-long role as a financial hub provides durable advantages: common law, deep pools of technical and financial talent, a sophisticated investor base, and ambitious entrepreneurs. While the ecosystem has yet to see major VC-scale exits or the formation of a “crypto mafia” of former employees, the tide is turning.

2025 has been a pivotal year. For the first time in nearly a decade, UK equity investment has decoupled from the price of Bitcoin. Despite Bitcoin reaching an all-time high of $126k on October 6, 2025, UK start-ups raised just £100m in the first half of the year—the lowest H1 total since 2020. While headline figures suggest a subdued market, the reality is more nuanced: capital is shifting toward fundamentals, not fads.

Seasoned venture investors know that generational companies are built in challenging markets. Beyond funding headwinds, the UK faces structural barriers—slow regulatory progress, limited banking access, an absence of native layer-one protocols (Aave being the exception) and their network effects, a complex tax environment, and a shortage of specialist domestic capital.

Yet at AlbionVC, we remain optimistic. The UK has the ingredients to build and scale global leaders in institutional-grade digital assets. The country already hosts category leaders such as Blockchain.com in trading infrastructure and Copper in institutional custody. B2B infrastructure firms in this space operate with 70% gross margins, long-term contracts, high switching costs, and growing regulatory moats.

Within our own portfolio, companies such as Elliptic (blockchain analytics), OpenTrade (stablecoin yield infrastructure), and Agio Ratings (risk management) exemplify the UK’s potential to create global outliers.

A strategic specialisation, focused on institutional-grade infrastructure, is where the UK can become a global champion. The UK has repeatedly proven its strength in building backbone infrastructure for institutional markets. With its common law framework, global financial credibility, and recent landmark developments — such as the LSE’s Digital Market Infrastructure platform integrating blockchain into mainstream finance— the UK is uniquely positioned to lead the next wave of institutional digital asset innovation.

If you are building or investing in this space, we’d love to hear from you.

The three distinct periods of UK crypto

The past decade has been marked by periods of volatility and change, but also by an establishment of a vibrant ecosystem. In our mind this transition can be split into three distinct periods:

- Early UK ecosystem was dominated by B2C startups – 55% deals done

- Most B2B companies were building within capital markets and payment sectors. This is due to the initial focus on building the transactional infrastructure needed to enable trading and the movement of value

- Total amount raised £81m from local VCs and angels

- Dominated by deals under £2m, except for Blockchain.com that in June 2017 raised £31.5m —the first UK digital asset deal above £30m

- In 2018 more deals were done than in the entire Phase 1 – 59 vs 53, with corporate investors becoming active market participants and from 2019 onwards crypto native firms started to venture invest

- In 2022 £713m was raised, catalysed by the UK “tech hub” policy, stablecoins recognition, FMI sandbox and rising US participation including a16z expansion to London

- From 2021 onwards, rounds over £10m became a regular feature. This trend coincided with a sharp increase in participation from US and other international investors

- In 2021 alone £625m was raised across 103 deals, helped by two landmark rounds at Blockchain.com that together made up over a third of the year’s total

- 2023/4 reset years as investment levels came down post market highest, but remained above the pre-boom years

- Sub £2m deals on the decline, with growth rounds active during the reset phase

- £378m raised in 2023, then +26% YoY in 2024 despite a 9.4% fall in the wider equity market

- Capital concentrated in a fewer winners – 3 companies raised >£100m

- By 2025 infrastructure and banking segments consolidated advantage with the highest average amount raised per deal

- By the end of H1 2025 UK ecosystem decoupled from the price of Bitcoin – contrast with Bitcoin price at all time high vs the slowest equity investment amounts in H1 since 2020

01

Investment landscape

UK digital assets investment matures after years of rapid expansion

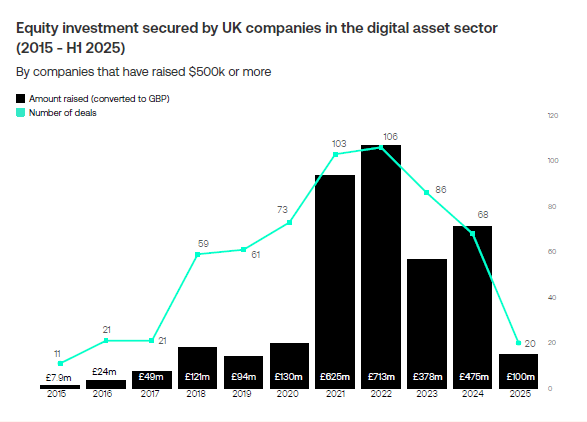

Equity investment in UK digital assets companies has grown substantially over the past decade to

£2.7bn, though recent data suggest the market

is entering a more measured phase after a period of exuberant growth.

![]() From modest beginnings — just £7.9mn raised across 11 deals in 2015 — the sector expanded rapidly. In 2021, companies in the sector raised a total of £625m via 103 deals, marking an almost fivefold increase in funding from 2020. A major contributor was Blockchain.com, the London-based cryptocurrency wallet and data platform. It closed two landmark rounds that year: £86.5m in February and £218m in March, together accounting for 49% of all capital raised in the sector in 2021.

From modest beginnings — just £7.9mn raised across 11 deals in 2015 — the sector expanded rapidly. In 2021, companies in the sector raised a total of £625m via 103 deals, marking an almost fivefold increase in funding from 2020. A major contributor was Blockchain.com, the London-based cryptocurrency wallet and data platform. It closed two landmark rounds that year: £86.5m in February and £218m in March, together accounting for 49% of all capital raised in the sector in 2021.

Annual investment peaked at £713m in 2022, spread across a record 106 deals, before moderating to £475m in 2024.

x

x

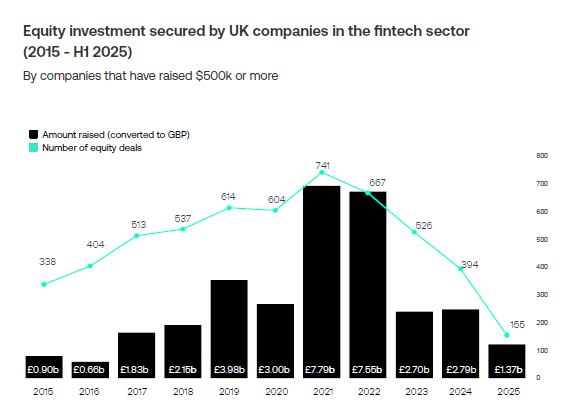

The fintech equity market has followed a similar pattern over the last 10 years, with a sharp rise in 2021 and 2022 followed by a reduction in 2023. The scale of capital raised underlines fintech’s greater maturity relative to digital assets.

In 2024, the wider equity market saw a 9.4% year-on-year decrease. Companies in the digital assets sector were resilient to this, with a 26% increase in funding. However, the first half of 2025 has seen a slow start with deal value reaching £100m – the lowest H1 figures since 2020.

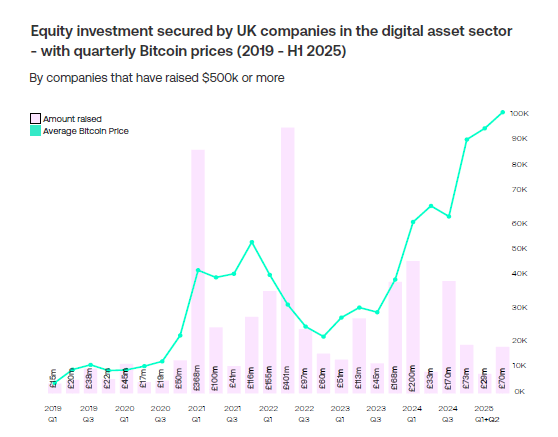

Equity investment and Bitcoin price

From 2019 through 2020, equity funding remained modest, with quarterly raises rarely exceeding £40m. Bitcoin traded below $15k during most of this period, reflecting a cautious investment environment with limited institutional interest. Momentum shifted sharply in 2021 as investment activity surged in Q1 (£368m), tracking closely with Bitcoin’s breakout above $30k. The Bitcoin crash from the highs of Q4 2021 to the lows of Q4 2022 coincided with a reduction in digital assets investment, albeit with a slight lag. During Bitcoin’s recovery from Q4 2022 to Q1 2024, digital assets companies experienced higher investment values.

This correlation does not continue into 2025. Despite Bitcoin reaching record highs, investment into UK digital asset companies has not followed the same trajectory. The Bitcoin price boom has been attributed to the favourable regulation being brought in the US (the GENIUS Act). The slow start in H1 2025 raises the question of whether investors are holding back ahead of new UK rules on digital asset firms.

x

Why the UK’s decoupling from the

Bitcoin price matters

Decoupling of Bitcoin’s price from UK deal flow is a double-edged signal. On the positive side, it

suggests capital is starting to chase fundamentals rather than momentum: investors are prioritising regulated revenue, enterprise contracts and defensible IP over trading exposure. The bar for raising equity funding is higher thus capital is flowing to sustainable business models rather than short term trends. This is a positive trend on backing companies with solid business models and thus potential to endure and win over the long-term.

The flip side is a funding gap. If price rallies no longer pull in generalist US capital, UK startups become more reliant on a domestic and European stack of seed-to-growth investors. While European investors have become increasingly more active across the UK ecosystem in recent years, their numbers do not make up for the

xxx

US investor pull out. Without it, founders face longer fundraises, flatter valuations and stronger covenants. Some may choose to relocate to jurisdictions where capital is deeper.

There is a contrarian view that we at AlbionVC share that today’s generation of digital assets companies are operating with a global mindset, global customers and investors from day one. Thus decoupling is less of a concern for outlier founders who are able to raise investor interest in lower liquidity environment. of markets.

A recent example in our portfolio is OpenTrade, offering an institutional grade platform for yield products, who with their globally distributed team service customers across Latin America, Asia and Europe, have raised funding in H1 2025 from leading European and US investors including us at AlbionVC, a16z and Notion Capital. The latest round took place less than 6 months after their previous raise.

For UK policymakers, decoupling should raise alarm bells. Quality capital needs long-term clarity and a functioning sandbox, the pressure to get the rules right and quickly is on.

“With over $300 trillion in market cap, stablecoins are rapidly becoming the foundation of global financial infrastructure. At OpenTrade we’re seeing wallets replace traditional bank accounts and yield products bring real value to users worldwide. The next five years will be transformative with stablecoins moving from the edges of fintech into the core of how money actually moves worldwide.”

David Sutter, CEO & Co-founder, OpenTrade

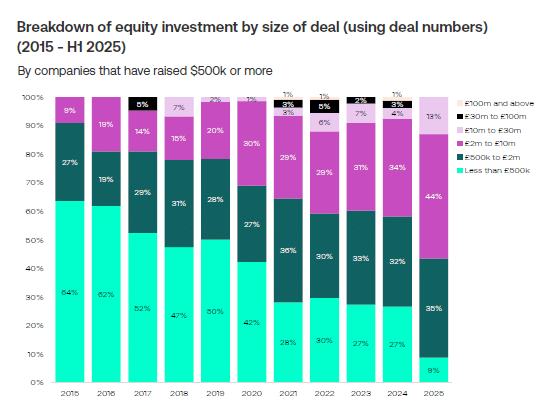

Breakdown of deals by size

In the early years (2015–2016), the market was dominated by smaller rounds. No deals above £5m were recorded in 2015, and rounds between £500k and £2m consistently accounted for at least a quarter of activity, with the exception of 2016 (19%).

By 2017, larger transactions began to emerge, including Blockchain.com’s £31.5m raise in June—the first UK digital asset deal above £30m. From 2021 onwards, rounds over £10m became a regular feature. This trend coincided with a sharp increase in participation from US and other international investors (see page 14).

Between 2021 and 2024, three companies collectively raised more than £100m each in equity: Blockchain.com, Copper, and Exohood Labs. These landmark raises highlight the transition of the sector to deals of a scale comparable with more established parts of the fintech ecosystem.

x

“The shift from small, early rounds to frequent large-scale raises shows how the sector has developed, with UK digital asset firms now viewed as credible late-stage investment opportunities rather than experimental startups.”

Jay Wilson, Partner AlbionVC

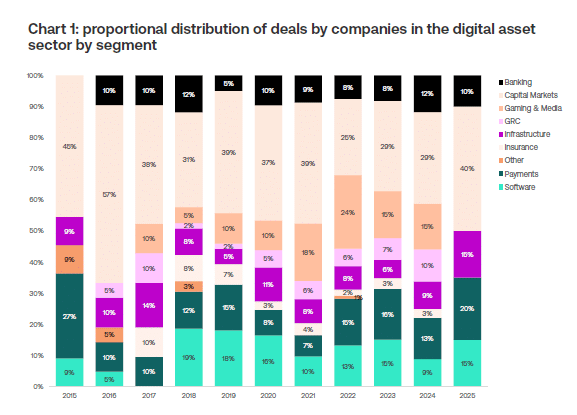

Breakdown of deals by sector and stage

In the early years (2015–2020), the number of deals within the digital assets sector was highly concentrated, with the capital markets and payments sectors together accounting for the majority of deals. This may be due to the sector’s initial focus on building the transactional infrastructure needed to enable trading and the movement of value.

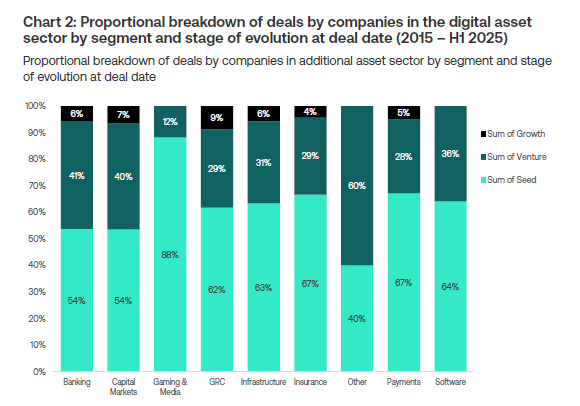

At the time, deal-making also skewed heavily toward the earliest stages: in 2015, more than 80% of deals were seed-stage, and even by 2018–2019, over 70% of activity was still concentrated at seed. The high proportion of early-stage deals reflects both the early stages of the sector and the phase of experimentation observed in this period.

From 2018, the landscape diversified. Software, infrastructure, and insurance emerged more prominently. This period also marked a clear shift toward companies within the Governance, Risk & Compliance segment, reflecting both the institutionalisation of digital assets and the regulation needed for their wider adoption.

x

“We continue to see a significant opportunity for digital-asset-native companies to build the critical infrastructure connecting TradFi and digital assets. Our 2025 investment in Agio Ratings, a best-in-class risk management platform for digital assets designed for banks, funds, and insurers, underscores our thesis: institutional adoption will be driven by trust, transparency, and robust infrastructure.”

Ana De Sousa, CEO Agio Ratings

As of 2024, the balance has shifted away from seed and toward later rounds. Seed now accounts for 58.0% of deals (down from 81.8% a decade earlier), while venture makes up 37.0% of the total number of deals secured by these firms.

Data for the first half of 2025 shows that 12.0% of deals by companies in the digital assets sector have been secured by growth-stage companies.

x

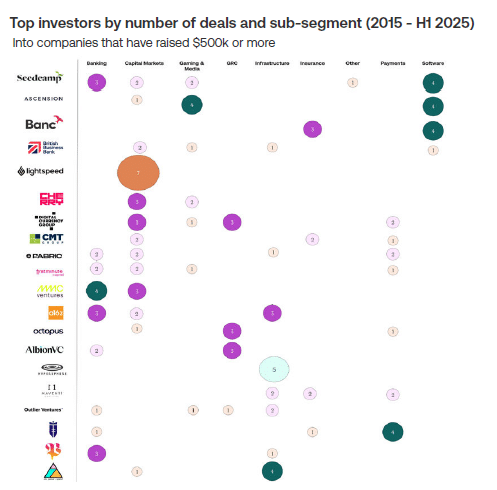

Investors

Seedcamp is the most active investor by deal count, reflecting its focus on early stage rounds across diverse sectors.

Larger US funds such as Andreessen Horowitz and Lightspeed are concentrated in infrastructure, banking and capital markets deals.

x

“We remain deeply excited about crypto infrastructure because it’s the foundation upon which the next generation of open, verifiable applications will be built. The evolution of blockchain infrastructure is transforming money & payments through stable coins and underpinning the safe & aligned adoption of AI. Those areas are where we at Fabric see generational value being created.”

Richard Muirhead, Managing Partner, Fabric Ventures

x

Investor geography

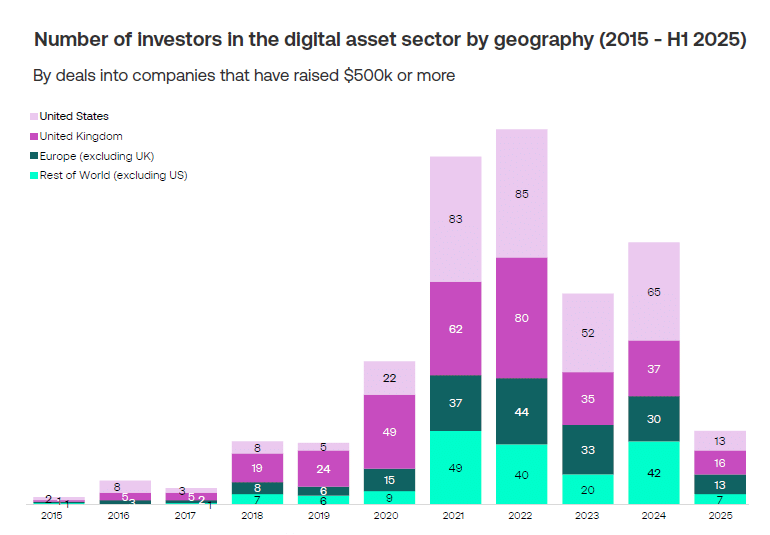

US and other international investors have become increasingly active in the UK digital assets market, a shift that has coincided with larger deal sizes.

Between 2017 and 2020, UK-based funds dominated activity, but from 2021 onwards participation from US and global investors rose sharply. This surge aligned with the record levels of capital raised in 2021 and 2022. Although overall investment has eased in recent years, US investors continue to participate at higher levels than those from any other country.![]() This reliance on US capital highlights both an opportunity and the need to deepen participation from UK and European investors, ensuring the sector’s growth and investment resilience is anchored on a broader base.

This reliance on US capital highlights both an opportunity and the need to deepen participation from UK and European investors, ensuring the sector’s growth and investment resilience is anchored on a broader base.

“As an enduring investor and operator of the crypto industry with over 250 investments across 40 countries, we continue to be excited by the opportunity to back the brightest minds to build the future of decentralised technology and fintech. As early backers of multiple UK startups we believe in the opportunity the region presents to create a better financial system.”

Richard Aseme, Investor, DCG

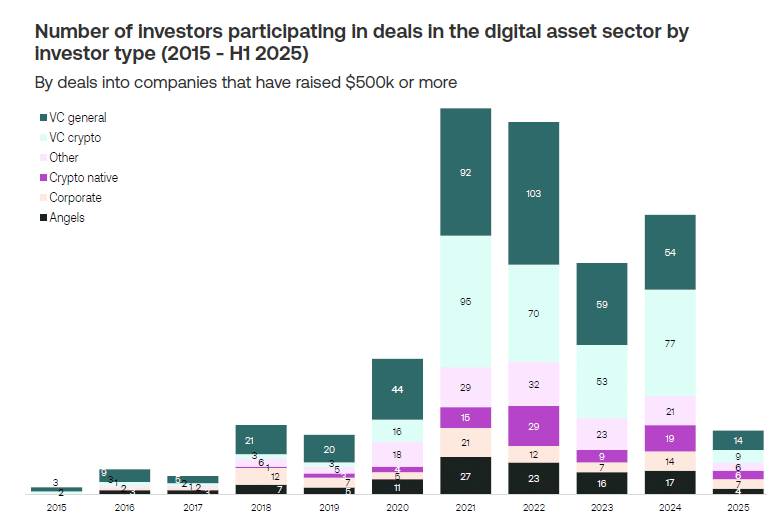

Investor type

Specialist capital driving sector growth

Generalist and crypto focused funds dominate digital asset dealmaking, together accounting for 45% of all investors active in the UK market (see methodology for investor type definitions).

The composition of these groups highlights the central role of US capital. Nearly half (46%) of all crypto-focused VC investors are US-based. The next highest proportion of this type is in the UK, at 8%. This highlights that the specialist capital driving much of the sector’s growth is concentrated in the US. By contrast, generalist VC funds are more evenly split, with 31% based in the UK and 29% in the US.![]() As the UK market expands, a deeper pool of specialist domestic firms could help reduce reliance on US capital and capture more of the value created in the sector. The past decade shows how quickly the market can evolve when international capital enters at scale. The next phase will hinge on whether the UK can broaden its investor mix.

As the UK market expands, a deeper pool of specialist domestic firms could help reduce reliance on US capital and capture more of the value created in the sector. The past decade shows how quickly the market can evolve when international capital enters at scale. The next phase will hinge on whether the UK can broaden its investor mix.

x

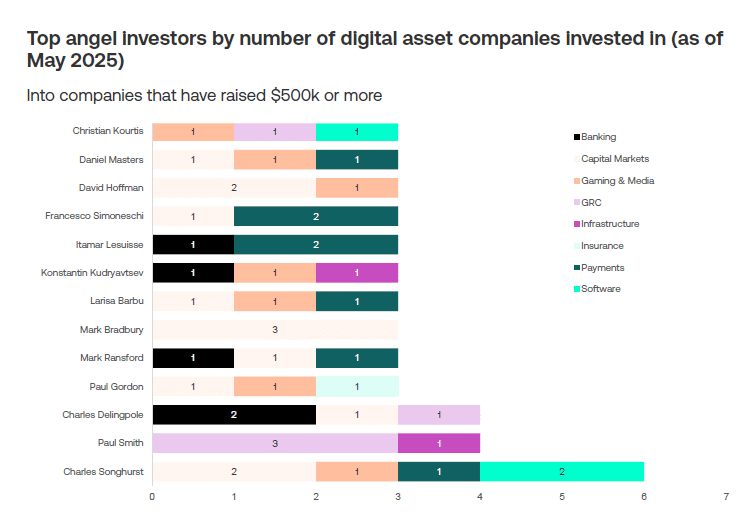

Angel investment

Individual angel investors are active across a range of sub-segments, with Charles Songhurst leading by deal count and showing the broadest spread. Others, such as Paul Smith and Charles Delingpole, are more concentrated in infrastructure and banking, while several investors focus tightly on capital markets.

x

02

Companies & Sub-segments

Top sub-segments by average amount

raised per deal

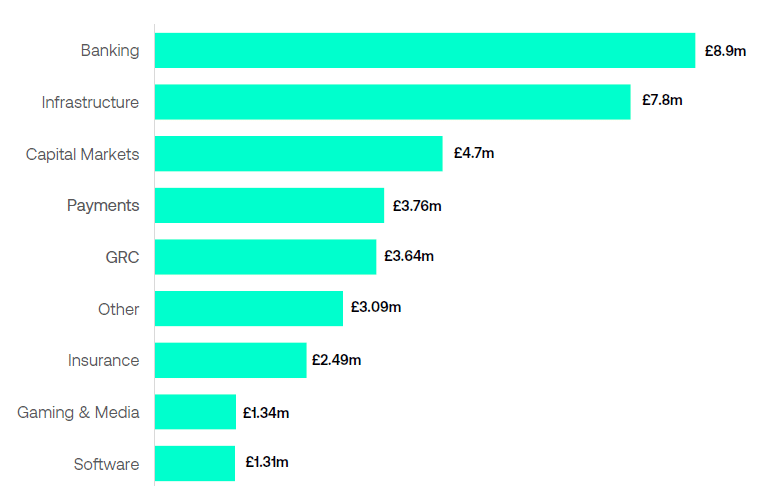

The Capital Markets sub-segment is the most prominent among companies in the digital assets sector, as well as a leader in equity fundraisings. Between 2015 and H1 2025, companies in this segment collectively raised £896m, followed by payments companies that have raised £354m and banking with £236m. Despite this dominance,

Capital Markets only ranks third in terms of average deal size. By contrast, Banking companies are at the top of the ranking, raising an average of £8.9m per deal.

Infrastructure companies come second with the average £7.8m per deal. Looking at the next graph (page 19) companies enabling institutional adoption of digital assets have a monopoly on where the top money actually goes. This is not surprising given strong unit economics – 70% growth margin, multi year contracts with painful

switching costs and thus sticky products, and regularly moats competitors can’t easily cross.

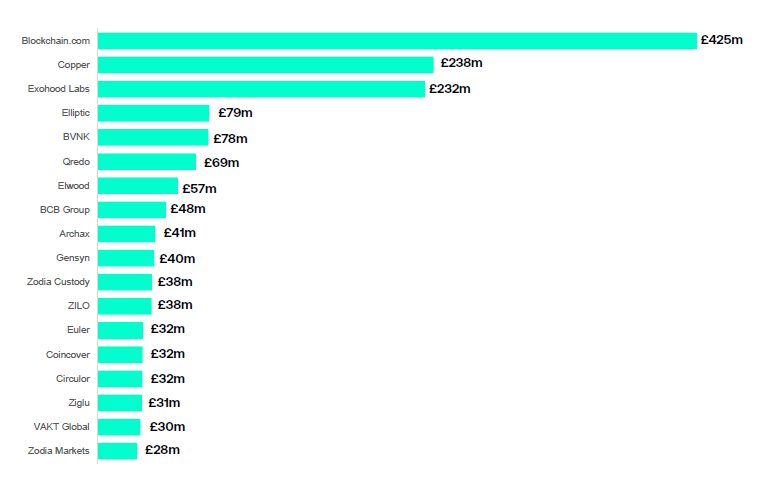

Top investment recipients

Within the digital assets sector, funding has become highly concentrated, in a small number of companies. While these firms have not necessarily secured a large volume of deals, the transactions they have closed are of exceptionally high value. The top three recipients illustrate this dynamic clearly.

Blockchain.com is a leading provider of digital asset trading and custody infrastructure, facilitating over $1 trillion in cumulative crypto transaction volume across retail and institutional channels. The platform operates with trading fees ranging from 0.00% to ~0.40% and sustains positive unit economics through transaction-driven revenue rather than token price exposure. With more than 90 million wallets created globally and over $15bn in institutional trading activity, Blockchain.com continues to expand its position as a core infrastructure provider bridging traditional finance and the digital asset ecosystem.

Copper is an institutional-grade digital asset custody and settlement platform, generating revenue primarily through 20–50 basis-point annual custody fees. Despite a decline in revenue from $27.7m in 2022 to $20.6m in 2023 during the crypto downturn, the company maintained a strong capital base and continued to expand its institutional client network.

While Copper posted a $60 million net loss in 2023 driven by customer acquisition costs, its revenue remains high-margin, reflecting the defensibility of its enterprise infrastructure model. Compared to consumer-facing dapps operating with low-margin, high-churn dynamics, Copper’s institutional focus positions it for stronger long-term profitability as digital asset markets mature.

Elliptic is a leading blockchain analytics and crypto risk management firm, providing compliance, investigation, and transaction-monitoring tools to financial institutions, crypto firms, and government agencies.

In July 2025, Elliptic reported that cross-chain criminal flows have surpassed $21 billion, underlining demand for sophisticated analytics across multiple blockchains. The firm continues to expand geographically — for example, opening a regional headquarters in the UAE in 2024.

To date Elliptic has raised £79m.

“Elliptic sits at the nexus of the digital asset market and the traditional financial system as they integrate -both need trusted intelligence to manage the associated risks. Backed by leading global investors, to date we’ve helped crypto businesses, governments, financial institutions, and regulators engage safely with digital assets, and our market opportunity continues to expand exponentially.”

Simone Maini, CEO Elliptic

03

Exits

Exits by year

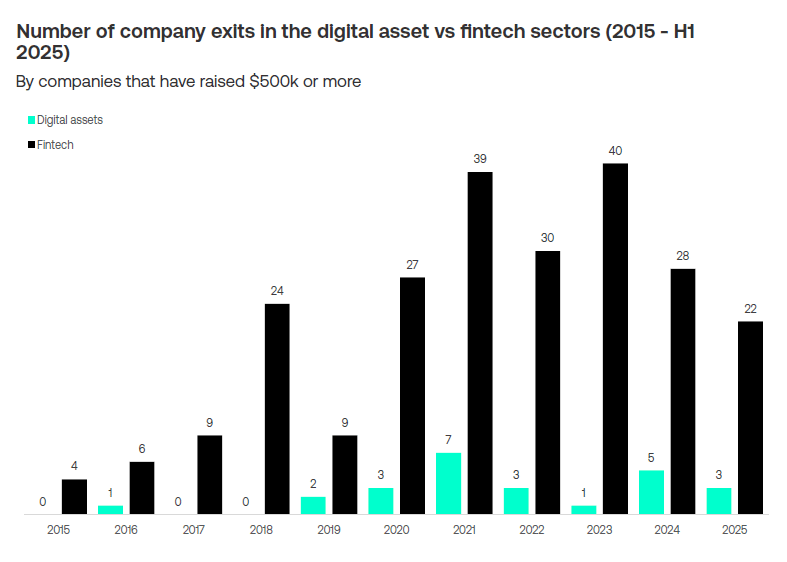

Over the past decade, there have been twenty-five UK digital asset exits, with only one IPO to date. Given how early the market remains relative to fintech, this limited exit activity is unsurprising—the talent and capital flywheel is still forming as UK growth-stage digital asset firms scale into global category leaders.

By contrast in the US ecosystem, which is further along the maturity curve, there have been a number of recent large acquisitions, such as Stripe acquiring Bridge for $1.1bn, Kraken acquiring Ninja Platform for $1.5bn, Ripple acquiring Hidden Road for $1.25bn.

x

Exits breakdown

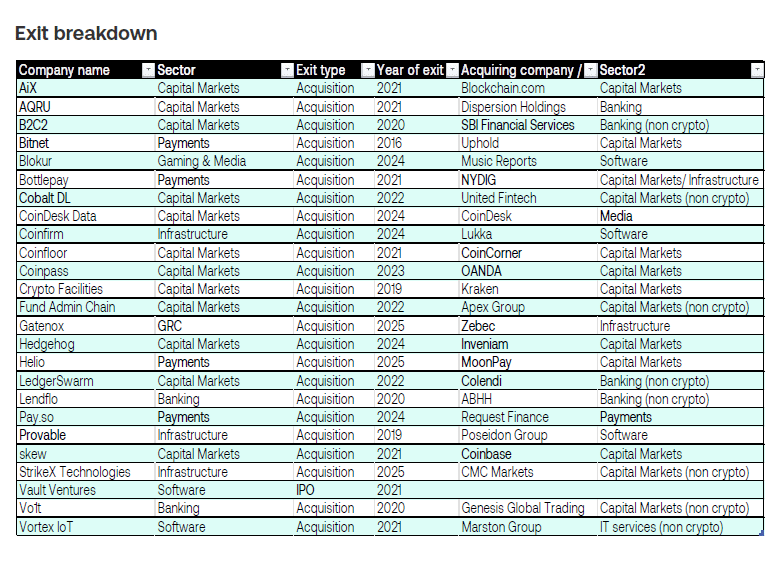

To date, most of UK M&A has been driven by US acquirers, underscoring the strength of UK innovation but also highlighting a risk of value leakage as talent and intellectual property are pulled abroad.

![]()

x

04

UK market fundamentals

This section of the report highlights structural market considerations for UK digital assets, outside of the investment landscape.

Regulatory framework: progress and perspective

Achievements

The Financial Conduct Authority (FCA)’s phased FSMA-based crypto regime, introduced in 2025 and expected to be implemented in 2026, consolidates oversight of exchanges, stablecoins, and custodians under a unified regulatory framework. The lifting of the four-year retail ban on crypto exchange-traded notes in October 2025 has reopened access to Bitcoin and Ether via mainstream venues such as the London Stock Exchange and Aquis, potentially unlocking up to £930 billion in tax-advantaged investment accounts.

The UK’s regulatory approach differs from the EU’s Markets in Crypto-Assets (MiCA) framework, which, while offering pan-European passporting across 27 markets, has faced slower implementation and limited flexibility. Post-Brexit, the UK’s ability to legislate independently enables flexible adaptation to emerging technologies—positioning it to lead innovation in digital asset regulation if it takes decisive steps.

Implementation Challenges

Despite progress, execution gaps remain. Consultations closed in July 2025, but final rules are not expected until 2026, with full authorisations extending into 2027—a 12–18 month timeline that lags peers. In contrast MiCA became fully operational in December 2024, Singapore’s Payment Services Act has been active since 2020, and Dubai’s Virtual Assets Regulatory Authority issues licences within 4–6 weeks.

Between 2020 and 2024, the FCA approved only ~50 of 359 applications (a 13% success rate), and we saw exits such as GlobalBlock’s relocation and a16z’s London office closure. While the FCA has shortened approval times from 17 to 5 months, signalling genuine progress, further acceleration is essential to build the UK ecosystem to be globally competitive.

Distribution infrastructure: promise meets practice

Theoretical Potential

The UK’s financial system includes approximately 40,000 FCA-regulated firms, offering unparalleled reach for digital-asset products. Early adopters such as challenger banks (Revolut and Monzo), payment specialists (Checkout.com and Wise), and wealth platforms (AJ Bell and Hargreaves

Lansdown) are experimenting with tokenised or crypto-linked offerings. For compliant startups, this infrastructure enables scaling through trusted channels rather than building retail credibility from scratch.

Practical Reality

In practice, fewer than 51 firms hold crypto-specific FCA registrations, with under 15 active retail platforms—including Kraken, Coinbase, and Crypto.com—forming the core of the UK’s distribution network. This limited retail infrastructure represents a material bottleneck to market expansion.

Banking access remains the sector’s most acute constraint. As of January 2025, around 50% of UK crypto firms reported account denials or closures. Major high-street banks maintain restrictive policies: NatWest caps daily crypto purchases at

£1,000, HSBC limits monthly volumes to £10,000, and Santander to £3,000. Some institutions have exited the sector entirely.

This stands in sharp contrast to jurisdictions such as Singapore, where DBS Bank operates a regulated digital asset exchange; Switzerland, home to crypto banks like Sygnum; and the UAE, where banks increasingly engage with digital assets under clear regulatory oversight. For UK firms, restricted banking access is not just an operational hurdle—it is an existential

challenge for maintaining payments and treasury operations. Encouragingly, new HM Treasury rules effective April 2026 will require banks to provide 90 days’ notice before account closures, offering greater operational certainty

Talent, technology and capital efficiency

Human Capital Advantages![]() The UK employs approximately 8% of the global crypto workforce and one-third of Europe’s blockchain talent—the largest share in Europe. Average blockchain developer salaries stand between £70,000 and £100,000 (with median salaries reaching £100,000, up 43% in one year),

The UK employs approximately 8% of the global crypto workforce and one-third of Europe’s blockchain talent—the largest share in Europe. Average blockchain developer salaries stand between £70,000 and £100,000 (with median salaries reaching £100,000, up 43% in one year),

roughly half the US equivalent. Combined with a cost of living 25-40% lower than San Francisco or New York, this provides UK companies significant capital-efficiency advantages.

The talent pipeline benefits from world-class institutions: the Alan Turing Institute, Oxford’s Cyber Security Centre, GCHQ-linked programmes in applied cryptography, and over 15 universities

offering specialised blockchain programmes. London has the world’s deepest institutional services ecosystem outside the United States.

Legal framework and institutional credibility

Human Capital Advantages![]() English common law continues to provide a solid foundation for innovation. Courts recognised crypto-assets as property in 2019, and the Digital Assets Bill 2025 codifies those rights.

English common law continues to provide a solid foundation for innovation. Courts recognised crypto-assets as property in 2019, and the Digital Assets Bill 2025 codifies those rights.

Unlike Europe’s civil-law systems, which rely on detailed statutes, common law evolves through precedent—making it inherently adaptive to new asset classes.

Alignment with US and EU sanctions, anti-money-laundering, and financial-crime standards gives London additional weight as a trusted jurisdiction for institutional adoption. Operating under a predictable, globally respected legal framework remains one of the UK’s quiet but enduring strengths, providing a natural competitive advantage in institutional services where legal certainty commands premium value.

Institutional adoption and infrastructure

The London Stock Exchange Group’s Digital Markets Infrastructure (DMI) platform, launched in September 2025, marks a pivotal step in integrating blockchain into mainstream finance. Its first tokenised fund settlement, powered by Microsoft Azure, enables end-to-end issuance, trading, and settlement of digital assets within regulated capital markets.

This positions London as the first major financial centre where both retail and institutional investors can access tokenised exposure through established venues. The DMI’s launch underscores a structural shift as global institutions adopt blockchain to streamline market infrastructure, reducing friction and cost across the asset lifecycle.

04

Summary

Building the next wave of UK digital asset leadership

Over the past decade, the UK’s digital asset ecosystem has evolved. From seed-stage experimentation to more than £2.7bn in equity capital having been raised across distinct growth phases, bringing the ecosystem to a pivotal juncture: how to leverage its potential and build durable,

world-class companies that define the next decade.

At AlbionVC, we believe the foundations for this next chapter are firmly in place. The UK’s proven fintech track record and London’s

status as a global financial hub provide a strong launchpad for digital asset leadership. Progress on regulation and institutional adoption is emerging but maintaining competitiveness will require urgency to match international markets that have moved faster. The US’s GENIUS Act has established federal clarity for stablecoins, Europe’s MiCA framework

has unified the bloc under a single digital asset regime, and Singapore’s Payment Services Act has created a trusted, institution-first model. Each of these frameworks has advanced legitimacy while narrowing space for unregulated actors. The FCA’s recent steps are encouraging, but acceleration is essential if the UK is to lead rather than follow.

Data points to a market undergoing structural maturation. Capital has become increasingly concentrated in established category leaders (top three companies raised £895m), potentially leaving a gap at the early stages. Business models are shifting from consumer-facing apps to resilient B2B infrastructure, an area where the UK has already produced standout companies such as 29 Copper (institutional grade custody), Elliptic (crypto compliance) and BVNK (stablecoin infrastructure). In 2025, investment in the sector has moved beyond Bitcoin price cycles, shifting towards utility, fundamentals, and credible use cases in areas such as stablecoins and decentralised finance, alongside growing engagement from financial institutions, governments and regulators.

Investor dynamics are evolving in parallel. The pullback of specialist US capital has been partially offset by domestic and European investors stepping up, while generalist funds are increasingly complementing the crypto-native investor base. The UK also benefits from a growing angel ecosystem, set to accelerate as liquidity events begin to seed a new generation of experienced operators turned angels. Although the exit environment remains less mature than in the United States, early M&A activity (25 exits to date in the UK), multiple $1bn+ exits across the Atlantic and a cohort of mature companies that should seek liquidity in the not too distant future, suggest that things are about to change —an essential development for recycling capital, talent and ambition.

Our own investment track record (four investments completed over the past 12 months), underscores our conviction in visionary UK founders who are bridging traditional finance and the crypto economy. Institutional-grade infrastructure and regulated use cases represent the most compelling opportunities ahead, areas where the UK already demonstrates global strength and is well placed to define the future of digital assets. London has reinvented itself for centuries, from financing global trade to pioneering the Eurodollar market to dominating FX. Digital assets represent the next frontier in that legacy. With 35% of UK adults now engaged with digital assets, the decision to participate has been made. .

The question is no longer if the UK will engage but how: will it lead, follow, or merely facilitate others’ leadership? Our analysis shows that with focused reform and continued momentum, the UK can win on the global stage. The opportunity to shape global digital asset infrastructure exists today but will not remain open indefinitely. If you are building or thinking of building institutional infrastructure for digital assets, we would love to hear from you

At AlbionVC, we believe the foundations for this next chapter are firmly in place. The UK’s proven fintech track record and London’s status as a global financial hub provide a strong launchpad for digital asset leadership.

Methodology

The definitions below are used to group companies within the following digital asset subsegments:

• Banking

• Capital Markets

• Gaming & Media

• GRC

• Infrastructure

• Insurance

• Other

• Payments

• Software

Core criteria for companies:

• Founded in or after 2015

• UK HQ

.

The following definitions have been used to define investor types:

• Angels – angel investors

• Corporate – large corporates

• Crypto native – firms whose core business is focused on digital assets

• Other

• VC Crypto – venture capital firms focused on investing in digital assets and blockchain

• VC General – generalist venture capital investors

To be included in our analysis, any investment must be:

• Some form of equity investment

• Secured by a non-listed UK company

• Issued between 1 January 2015 and 30

• June 2025