European HealthTech Market Map 2022

by Sean Hewetson, Molly Gilmartin, Christoph Ruedig

Posted

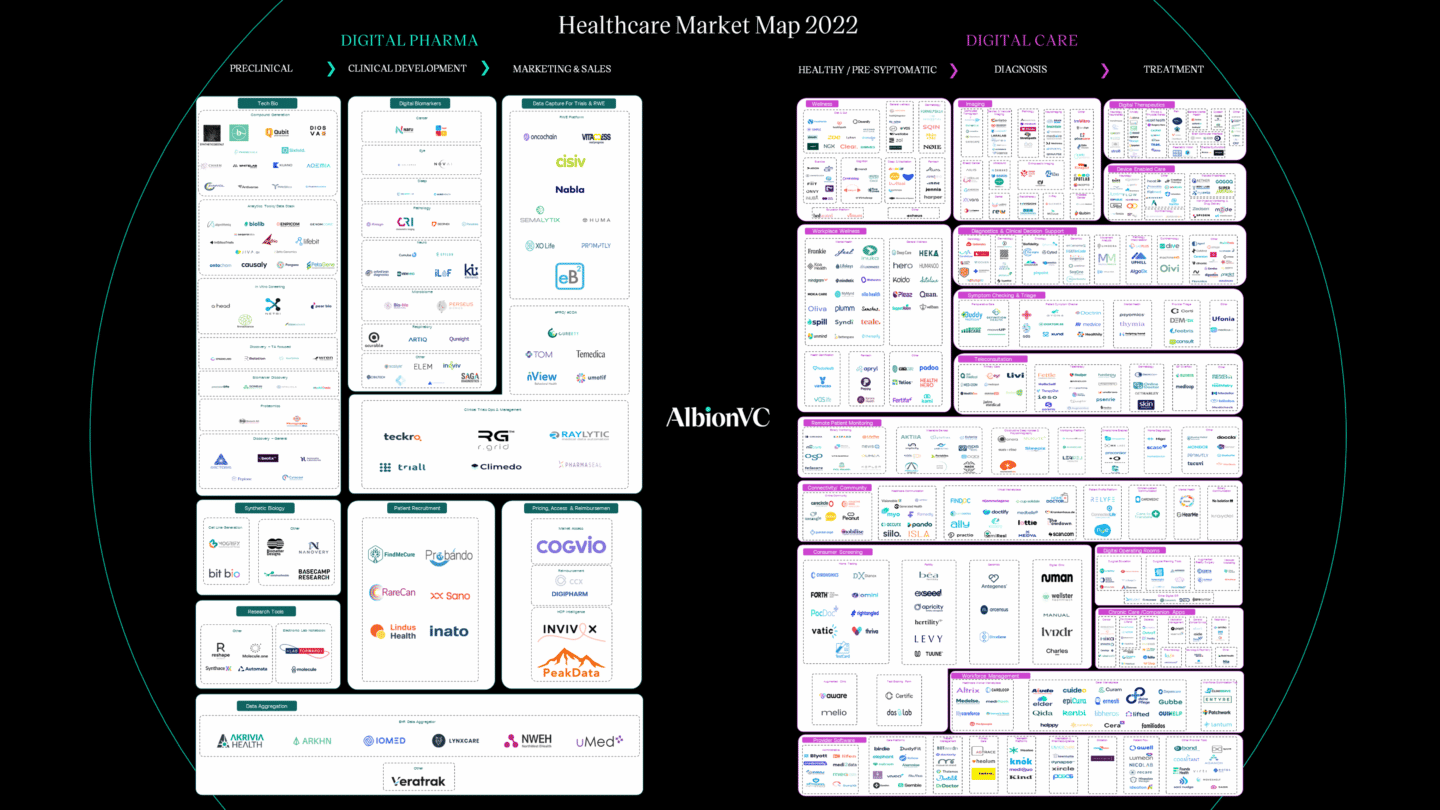

Market Map of the leading European healthcare companies

In early 2021, we published the AlbionVC HealthTech Primer and the first European HealthTech Market map. At the time, we felt that the European ecosystem of health technology startups and scale-ups was being overlooked as large headline-grabbing funding rounds were reported on an almost daily basis by American companies. A lot has changed since.

We have learned to live with Covid-19 and some of the pressures from the pandemic on the healthcare and life sciences industries have eased. Perhaps more importantly, the growth in venture funding seen over the last few years has gone heavily into reverse, and we face surging inflation and an impending recession. What hasn’t changed, though, is the entrepreneurial spirit and mission drive of founders in Europe seeking to fix what they see as broken healthcare systems. As we explained in the Primer, Covid-19 has been a catalyst that has driven rapid adoption of technology by patients, providers and pharmaceutical companies and the change is here to stay. The healthtech market has grown and so has the universe of European healthtech startups and scale-ups.

In putting together the European HealthTech Market Map 2022, we have taken a different approach to 2021. Rather than focussing on selected, mostly later-stage companies, we endeavoured to scan all European health technology companies that fulfilled a set of criteria (listed below in methodology section). The result is what we hope to be a fairly complete picture of healthtech startups and scale-ups that shows the richness of the European ecosystem.

For consistency, we have maintained the segmentation used in the 2021 market map. However, we are noticing a trend of the borders between segments starting to blur. An example of this are companies that focus on digital biomarkers, which in our market map may fall under the imaging, chronic care, companion apps, digital therapeutics, and diagnostics and clinical decision support sectors in the broader digital care segment. Yet, these companies may be monetising their technology mostly via the pharmaceutical industry, which needs biomarkers for clinical studies and so could be classed under digital pharma. Other examples are companies focusing on “Real World Evidence” generation, which are developing products around data collection and aggregation across both the digital care and digital pharma segments.

As the healthcare market continues to mature, we’ll see further blurring of lines between digital care and digital pharma, and within them. As the sectors continue to evolve and new ones emerge, we expect to see the creation of new business models that give rise to global category leaders.

As the healthcare ecosystem continues to evolve our market map will keep changing.

Download HealthTech Market Map 2022 here or explore the digital version below.

Wellness

Teleconsultation

Provider software

Consumer screening

Chronic care & companion apps

Connectivity and community

Workplace wellness

Symptom checking and triage

Remote patient monitoring

Diagnostics and clinical decision support

Imaging

Digital therapeutics

Workforce management

Device enabled care

Digital operating room

We are noticing a trend of the borders between digital care and digital pharma segments starting to blur. In the long-term this will give rise to new business models and lead to the creation of European healthcare category leaders globally.

Christoph Ruedig, Partner AlbionVC

Tech bio

Data capture for trials and RWE

Research tools

Patient recruitment

Pricing, access and reimbursement

Synthetic biology

Digital biomarkers

Data aggregation

Market Map Methodology

Criteria for inclusion of companies in the market map:

- Health technology companies (primarily software but can include elements of hardware and/or service) focused on the healthcare (providers, patients, regulators) or life sciences (pharma, medtech) industry;

- Founded in 2015 or later;

- With a European HQ;

- Which had raised an announced institutional funding round in the last three years;

- Had ten or more employees.

There were several companies we identified as market leaders which we have included in the market map for completeness though these did not meet all of the criteria listed above.

We partnered with Dealroom as our main database provider and utilized information from Beauhurst and Crunchbase to generate a list of these companies. Data was collected from 01/09/22 to 8/09/22. Following this, we examined each company in turn and applied exclusion criteria to focus in on companies where software was the driver of their business.[1]

We then allocated these companies to a taxonomy based on our 2021 analysis and expanded out areas that were over-represented. Within these groups, we tried to subgroup companies operating in a similar space together to better outline the different product areas. Where companies could have existed in multiple areas, we used our best judgement based on available information. All information for categorisation was collected from websites, supplemented with knowledge within the team.

If you think you should be included on this map or would like to update the information shown, then please fill in the form below.

[1] Exclusion criteria: online pharmacies, prescription management companies, supply chain/procurement companies, exclusively marketing or financial products for healthcare, COVID-19 testing companies, robotic surgery companies, insurance tech companies, employee benefits marketplaces, cannabis companies, industrial workplace risk management, agri-tech, veterinary tech, non informatics-based diagnostics/assays, cosmetics, supplement companies, personal trainer focused companies, devices (without user external connectivity (software in medical device), that are implantable, that are not readily mobile (new scanners etc.)), developers/tools for the development of digital health products, assay-based pathogen diagnostics, 3D printed prosthetics, therapeutic companies where software is not the core differentiator

HealthTech Market Map 2022 is, we hope, a complete picture of healthtech startups and scale-ups that shows the richness and potential of the European ecosystem.

Christoph Ruedig, Partner AlbionVC