What are the top ten mistakes founders make when pitching?

Perspective, by Paul Lehair

I recently gave a Masterclass presentation at CogX on the top 10 mistakes made when pitching, which I thought I would turn into a blog post. As an ex-CFO turned VC, I made many of these mistakes myself previously and so the goal is to give practical insights on the key topics investors focus on and on how to best speak their language to get their attention.

I should clarify that I will talk about pitching in a broad sense here, so not just the pitch deck or the pitch meeting, but the entire pitching process including what should happen before and after the pitch itself.

There could be many different ways to answer this question of course, but I will focus on what I believe are the most important topics as well as on some mistakes that I feel are not talked about enough. Let’s go!

#1 Not being prepared enough

Like other mistakes listed here, this will sound obvious and yet, many founders and teams could be better prepared for their pitching and their fundraising process. Being fully prepared will help you maximise your chances of success and create momentum, especially in today’s market, which is very binary.

Managing a fundraising process is like managing a sales pipeline and so you need to prepare accordingly at different levels: (1) before you start your process (have a list of your target leads and figure out the best way to approach them), (2) before you do a call (research the person/firm you are speaking to) and (3) have your info ready (not just your deck but a small data room including extra materials on your product, tech, go-to-market approach and forecasts plan).

I know it is easy to say for an investor but you want to make it easy for VCs to develop their investment case and to run their process. Always remember that you are in competition with other opportunities they are currently reviewing in their pipeline.

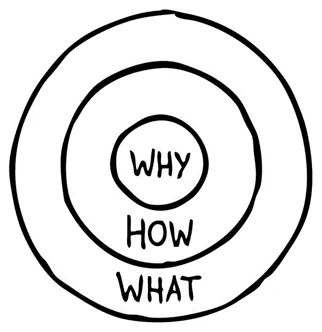

#2 Not starting with your company purpose

Be careful not to jump straight into talking about what you do (eg. “we are building a software for […]”), describing the solution and listing its features. As Simon Sinek would say, start with why. Make sure to step back and explain why your company exists, what is your company purpose and mission.

A broader takeaway here is that storytelling is a very important aspect of pitching: you want to be telling a clear story rather than just going through your pitch mechanically. Great storytellers are good fundraisers and storytelling is one of the key skills that investors assess during pitching.

#3 Not dumbing it down enough

Founders sometimes assume that people know their space and the problem they are solving. It can be natural as they are experts at what they do but as a result, they forget to give enough context about the sector they operate in.

It is best to assume by default that people do not know the basics and to explain very clearly topics such as: what is the current status quo of your space, what are the buyers’ problems, what are existing solutions, their pros/cons, how the market is segmented on they supply and demand side etc. Explaining things simply and giving clarity are attributes that are rarely displayed unfortunately.

#4 Not having a solid answer to ‘why now?’

This is one of the key questions that VCs are trying to wrap their head around because timing is one of the most important aspects of successful startups. There is typically a very good reason why the solution has not been created before and so the best companies have a clear answer to this (or why previous attemps were unsuccessful) and why now is the right time. A good way to address this topic would for instance highlitght new catalysts (eg. possibility to leverage newly created technologies, recent regulatory pressures etc.).

#5 Showing unreliable top-down TAM numbers

Showing huge top-down market size numbers (eg. “our TAM is a $10tn market”, to caricature the point) is not very useful. It risks making you lose credibility if you do not know granularly how this number is segmented on the supply and demand side.

It is much more convincing to show a bottom-up TAM based on (1) the number of prospects you can target (based on your ideal client profile or ICP) multiplied by (2) your average annual contract value (ACV or ARR/client).

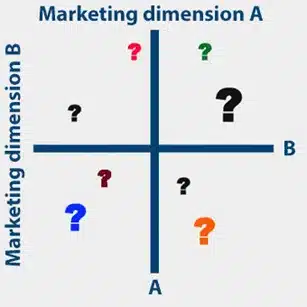

#6 Not describing your positioning clearly

You want to explain very crisply where you sit in the market in terms of (1) buyers segmentation (demand side) and (2) the competitive landscape (supply side). The goal is to show that you know your market (and your place within it) inside out.

There could be different ways to do this (via tables or diagrams) but make sure to answer key questions such as: What type of buyer segment (SME, mid-market, enterprise) are you addressing and why? What criteria are they using to make their decisions (time to value? ease of use? cloud-based vs on-prem)? How do you diffentiate and win vs competitors (in one crisp sentence ideally)?

#7 Not talking about defensibility

Defensibility is another key topic that investors focus on because enduring successful companies have strong ‘moats’ that protect them. You want to explain what is your key advantage vs others and how you will be able to maintain it over time.

If you are early, realistically you probably do not have a deep moat yet (unless you have unique IP, in which case you should definitely explain it), but that’s ok. What is key is showing that you are giving a lot of thought to defensibility and have a roadmap that will help continue defending your company going forward (by creating for instance network effects, or switching costs, or proprietary data etc.).

#8 Not telling your own story and your team’s

Sometimes founders do not spend enough time on introducing themselves and their personal story. Make sure to talk about your background and what experience and insights led you to create the company. Do the same for the key members of your team, highlighting anything that is unique about you and how complementary you are ideally. Investors invest first and foremost in founders and teams so make sure to spend enough time on this.

#9 Not asking questions to investors

Of course you will be the main one pitching and answering questions, but this is always a two-way conversation. Make sure to also ask questions and make VCs feel somewhat like they should be pitching to you too!

Good questions to ask could be: What is your experience or thesis in this space? How do you typically work with founders? What is your process / typical timeline? What will be next steps?

As the old adage says, getting a new investor onboard is like a marriage. You will therefore need to do your due diligence on them and show that you are being thoughtful about which partner you would like to add.

#10 Being slow

“I have almost never made money investing in founders who do not respond quickly to important emails.” Sam Altman

This might be controversial but make sure to be fast in your process. First, I would recommend to always follow up after a call/meeting (same day or next day). This will help you stand against other opportunities you are competing with. Remember that pitching is selling and about building relationships!

Second, high velocity is one of the key characteristics and advantages of startups. Your responsiveness will give investors a taste of your intensity as they will be assessing your pace throughout the process.

This actually takes us back to mistake #1: not being prepared enough. In order to be fast and to create momentum in your process, you need to be prepared with your information ready and in good shape.

Thanks for reading until the end if you have made it this far! I would love to get your feedback on plehair@albion.vc

Related content

Health x AI Hackaton

Join us for the Adeline 2026 Summer Sprint – a one day healthtech hackathon event, hosted in collaboration with AlbionVC, Google, Bupa & HSBC Innovation Banking.

UK’s Healthcare VC Scene in 2026 – Who’s Backing the Best Ideas?

AlbionVC listed as one of the most active and respected healthcare investors in Europe